Early Thoughts about 2017 Pulse Acreage

Farmers are already well into planning their 2017 crop mix and pulses will be included in many of their rotations. This year may not be as straightforward as just looking at which crops have the most attractive prices, as the good and bad production experiences from 2016 will also come into play.

In this report, we’ll take a few shots in the dark at potential 2017 seeded area. Because Canada is one of the major players in global pulse markets, we’ll also look at possible market implications. In doing this, we acknowledge that these are still just acreage guesstimates and the assumptions of average yields are even less certain. But as farmers nail down decisions, it’s helpful to have at least some initial ideas about 2017/18 market possibilities.

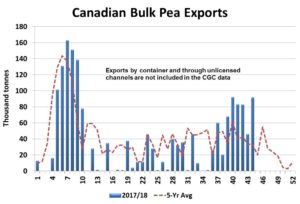

For most farmers, peas performed quite well in 2016 and that should provide some optimism about growing them again in 2017. True, new-crop bids are off from where they were last year at this time but at $7.00-7.50 per bushel, they’re still historically strong. Because of that, seeded area of peas will expand again this summer and set another new record, although the gain will likely be less than 5%.

Since yellow and green peas are two very distinct markets, it’s also important to consider how acreage of those two types could shift this spring. Historically, it’s taken a $1.50 (or more) per bushel premium for green peas to attract acres and that’s not the case (again) with this year’s new-crop bids. The last two years, production is shifted out of greens and into yellows and that will likely be the case again this year. The result is that (given average yields) green pea supplies will continue to tighten relative to yellows and that should reestablish a premium price.

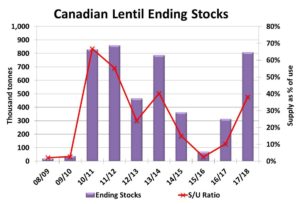

The outlook for lentil acres is a lot more complicated. New-crop bids are very attractive, especially green lentils at 35-40 cents (or more) per pound, and that should normally boost acres considerably. Even new-crop bids for reds are in the high 20s. The reality however is that plantings already jumped sharply last year to nearly six million acres, so it’s unclear how much further acreage could grow. More importantly, many lentil growers were left with a bad taste in the mouth as the crop struggled with wet conditions and diseases, and that will likely discourage 2017 acreage as farmers shift back to more normal rotations.

Our guesstimate for lentil plantings is a sizable 15% decline, but even that would leave seeded area close to five million acres, the second highest on record by a wide margin. The much higher new-crop bids for green lentils will bring more acreage back into those types (if seed can be found) and the majority of the decline would show up in reds.

Chickpea acreage will face some of the same influences as lentils. New-crop bids are exceptionally strong in the mid-40s for larger calibre kabulis, making it tempting for farmers to plant chickpeas again. But just like lentils, the challenging 2016 production year could discourage plantings as well. The net effect could be a modest drop in Canadian chickpea acres for 2017.

So far, new-crop bids for dry beans aren’t terribly attractive and that should cause a decline in seeded area as well. That’s especially the case in places where dry beans have to compete with soybeans for acreage.

Source : Albertapulse