By Scott Gerlt

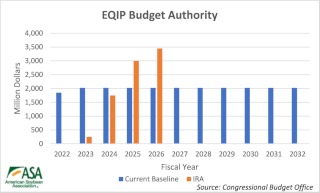

The IRA significantly expands several of USDA’s voluntary, incentive-based farm bill conservation programs to help address climate change. The Congressional Budget Office currently projects a budget authority for USDA conservation programs of $67.47 billion from 2022 to 2032 in the farm bill baseline. The IRA adds another $18.77 billion to that authority through fiscal year[1] (FY) 2026, specifically to help farmers adopt climate-smart agricultural practices.

- The program that has the largest funding injection is the Environmental Quality Incentives Program, which receives an additional $8.45 billion compared to a $22.10 billion baseline. The EQIP program provides a cost share to install conservation practices on ag land or nonindustrial private forestland. Most contracts are one to three years.

- The Conservation Stewardship Program provides assistance to maintain and improve existing conservation programs as well as adopt new practices. The entire farm must be enrolled, and contracts are for five years. The program was significantly changed in the 2018 Farm Bill, and budgetary authority for the previous version of the program ends in fiscal year 2023. The 2018 version has permanent baseline: The 2022 through 2032 baseline for the 2018-based program is $10.80 billion and the IRA provides $3.25 of additional funding.

- The Agricultural Conservation Easement Program provides easements for agricultural land and wetlands. The Agriculture Land Easements component prevents the conversion of enrolled land to nonagricultural use. ACEP has a baseline of $4.95 billion and receives another $1.40 billion through the IRA.

- The program with the largest relative infusion is the Regional Conservation Partnership Program. The RCCP provides funds for USDA to partner with organizations to implement programs proposed by applicants. The baseline for the program is $3.30 billion, and the IRA provides $4.95 billion.

The government fiscal year starts on October 1 of the preceding calendar year and ends on September 30th of the calendar year. For instance, fiscal year 2026 runs from October 1, 2025, to September 30, 2026.

While the preceding information outlines budget authority through FY26, that is only when the funds are committed, not necessarily spent. For these programs, USDA’s Natural Resources Conservation Service will implement producer contracts with the budget authority it has for each fiscal year, but the programs often disburse (outlay) annual payments over the contract period to producers. For practical purposes, USDA is simply committing the funds during the years specified in the IRA. In fact, $10.98 billion of the $15.31 billion in estimated outlays occurs in fiscal years 2027 to 2031. The estimated outlays are less in sum than the budget authority as some of the programs are subject to sequestration.

One very important issue must be kept in mind when comparing baseline spending to the funding in the IRA. While the baseline is permanent funding, the IRA funds are not. Senate rules prevent reconciliation bills from increasing the budget beyond a certain window, usually 10 years. As a result, reconciliation cannot be used to create permanent funding like the farm bill can. Therefore, under current law, the IRA funds are a one-time infusion that doesn’t directly add baseline for the farm bill. However, the funds do potentially provide an offset that could be used to establish permanent baseline in the farm bill, even if the money stayed in the conservation programs.

The IRA provides additional budget authority of $1.40 billion for conservation in addition to the programs outlined above. Of this, $1.00 billion is for NRCS to provide technical assistance to growers and other stakeholders. Another portion ($300 million) is available for NRCS to collect field-based data to quantify carbon sequestration from conservation practices, and an additional $100 million is set aside for administration of the programs.

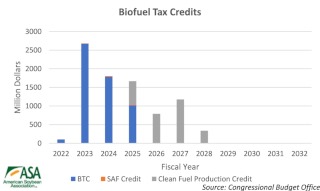

The reconciliation package also included provisions for biofuels. The Biodiesel Tax Credit provides a $1 per biofuel gallon tax credit to entities that blend renewable diesel or biodiesel with petroleum diesel. The provision was set to expire at the end of 2022 but is now extended until the end of 2024. The IRA also creates a sustainable aviation fuel credit in calendar years 2023 and 2024. It provides a credit of $1.25 plus $.01 per each percent of lifecycle greenhouse gas emissions reduction below 50%. In other words, SAF with a 60% GHG emission reduction would receive a credit of $1.35. The total credit cannot exceed $1.75 per gallon.

While the conservation provisions of the IRA provide fixed spending levels, the biofuel credit provisions provide just payment rates. The CBO estimated what they thought the actual spending levels would be by fiscal year. The standalone SAF credit is projected to cost $49 million over the two calendar years of the program. This would correspond to no more than 40 million gallons of production over those years. The BTC would produce credits of about $5.57 billion over two calendar years, and the CFPC would total about $2.95 billion over three. While we don’t know CBO’s underlying assumptions about trends in biofuel consumption, a primary reason for the lower spending per year is likely that the payment rates are expected to be less during that period. Only if a pathway had an emission score of 0 would it continue to receive the same payment rate as it did in the 2023 and 2024 period.

Another biofuel-related measure included in reconciliation is the Biofuel Infrastructure and Agriculture Product Market Expansion. This provides $500 million through September 30, 2031, to provide grants to improve infrastructure—outside of production facilities—for the sale and use of agricultural commodity-based fuels. Eligible fuel infrastructure for the grant includes biodiesel, home heating oil and ethanol.

Click here to see more...