By Dr. Todd D. Davis

Extension Grain Marketing Specialist

The November WASDE made minor changes to the 2017-18 wheat supply and demand projections, which is typical as there is little new production or demand information until the “final” estimates in January.

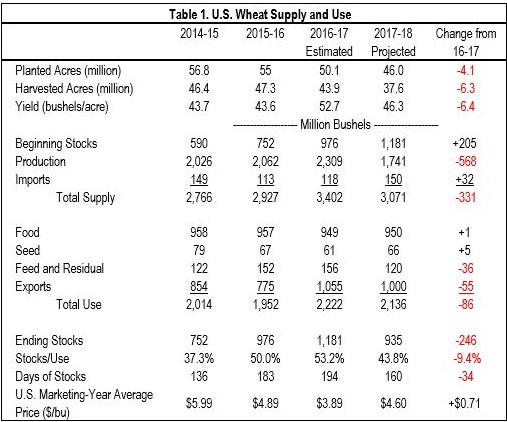

Harvested wheat area declined by 6.3 million acres from last year and about 10 million acres from the 2015 crop (Table 1). Last year wheat planted area fell by 4.9 million acres from 2015 but above average yields offset the impact of acreage reduction. This year Mother Nature provided the much-needed smaller yield that was 6.4 bushels/acre less than 2016’s yield. The 2017 wheat crop was 568 million bushels less than the 2016 crop. Because of stagnant demand, the 2017 carry-in of 1.18 billion bushels was 205 million bushels more than the previous year. Including imports, the 2017 wheat supply is 3.07 billion bushels, which is 331 million bushels less than 2016 (Table 1).

The problem with the wheat market has been slow growth in demand. USDA pegs food use at 950 million bushels, which only grows with population. USDA projects feed use to be slightly lower than last year and reflects the abundance of corn available for feed. The wildcard remains in the export market, which is projected to be 55 million bushels less than last year’s exports (Table 1).

USDA projects the 2017-18 ending stocks to decline to 935 million bushels. This decline is a result of attrition on the production side of the balance sheet and not growth in domestic or export demand. The road to higher prices will require stocks to decline from increasing demand for prices to return to higher levels. This year reminds us that a weather-driven supply shock that provides a one-year decline in stocks which supports higher prices. Typically, the next year’s crop is large enough to rebuild stocks and pressure prices lower.

USDA projects the 2017 U.S. marketing year average farm price at $4.60 per bushel for all types of wheat. Digging deeper into the numbers shows that the higher price is from production problems for the other classes of wheat. USDA projects soft red winter wheat stocks have increased from last year. In contrast, USDA projects all other wheat classes to have lower stocks. Because USDA aggregates wheat, the production problems elsewhere are showing a higher than expected wheat price from last year (Table 1). USDA projects the wheat inventory is to fall below a 50% stocks-to-use ratio for the first time since 2014.

USDA Releases Preliminary Long-Term Projections USDA also provided their initial market projections for the next ten-year period in late November for the major agronomic crop. This baseline projection is a product of economist computer models and does not include any information from farmers. Congress uses this information in their budgetary process, but it provides some insight into the long-term prospects for the grain markets.

USDA projects 2018-19 harvested wheat area at 38.3 million acres, which would be a 700 thousand acre increase from 2017 (Table 2). USDA also assumes trend yields, which would produce a 1.8 billion bushel wheat crop. Because of smaller carry-in and reduced imports, USDA projects total supply to decrease over the next three years. Less supply should support higher prices.

Unfortunately, USDA does not project demand growth. Total use is projected to be lower than this year’s projections for the next three years. Wheat exports are projected to muddle around the current level for the next three marketing years. The export problems will keep demand stagnant.

The discouraging part of these projections is that the decrease in wheat stocks for the next three years is from the impact of the smaller 2017 wheat crop.

Click here to see more...