By Hudu Abukari and Kevin Kim et.al

Agricultural and forest land are essential components of the rural economy throughout the southern United States. These lands support crop and livestock production, timber, recreational uses, and long-term investment opportunities. As regional demand for agricultural land continues to evolve, understanding who is buying land and how land-use patterns are shifting is increasingly important for producers, lenders, Extension agents, and policymakers.

In our previous Southern Ag Today article, we showed that individuals and general partnerships (GPs) remain the most active participants in the farmland market in terms of transaction frequency. However, there was an increase in the number of non-individual/non-GP buyers, particularly financial and real estate developers. In this publication, we dig deeper into more specific land types and buyer trends across southern states.

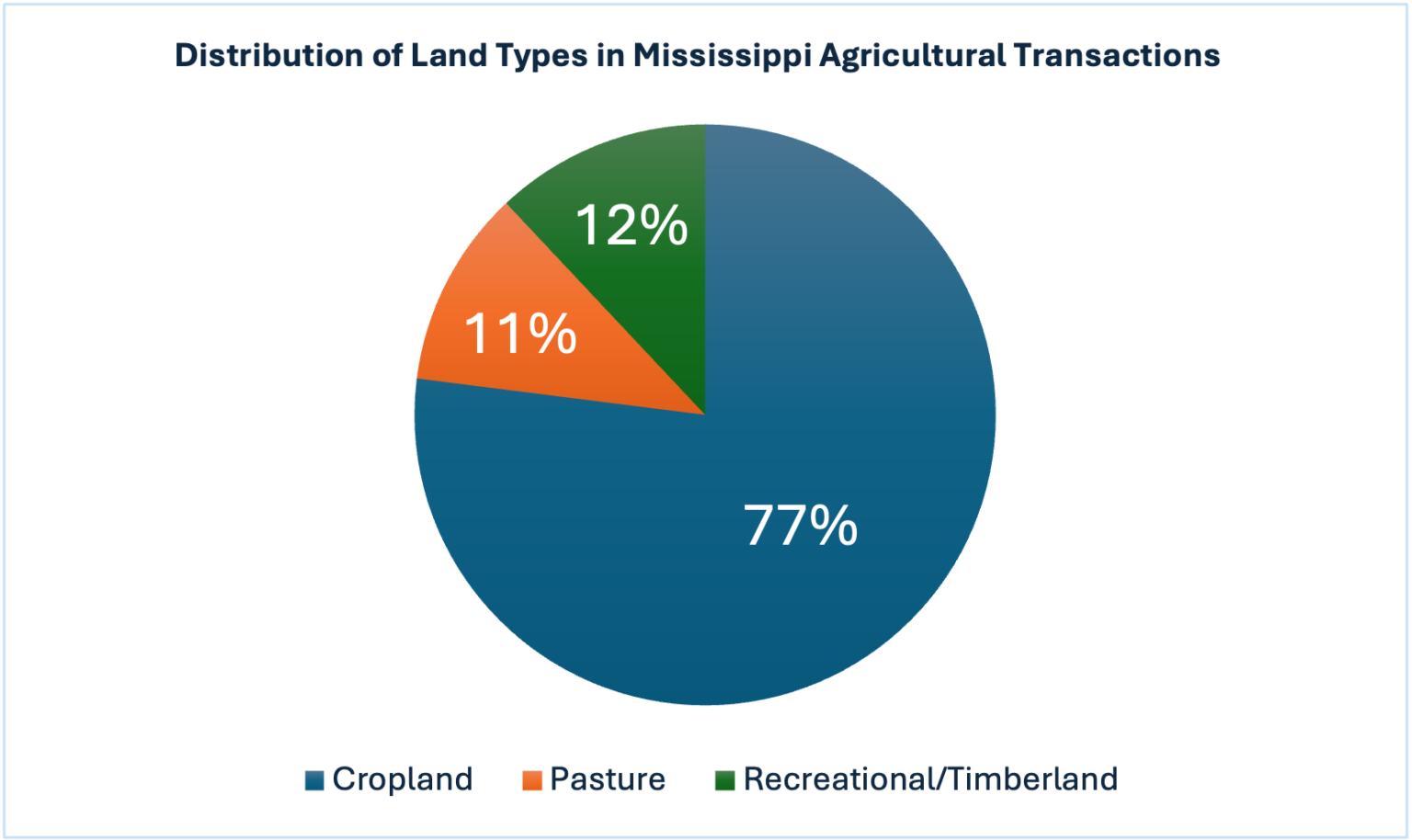

The majority of land transactions involve recreational/timberland, which accounted for 77% of all agricultural land purchases between 2019 and early 2023. Timberland dominates the rural landscape in many parts of the South, and its large share of transactions reflects its availability and investment appeal. In contrast, cropland represented only 11% of agricultural land transactions, while pasture made up the remaining portion in terms of transactions. This difference highlights a key challenge in many southern markets: cropland and pasture turnover is relatively low, while timber and mixed timber-recreational tracts are far more commonly available.

Types of Buyers Participating in Different Agricultural Land Market

Buyers of agricultural property generally fall into four categories: (1) Individuals and general partnerships (GPs); (2) Non-individual/non-GP agricultural businesses; (3) Financial and real estate businesses; and (4) Other industries. A closer look shows distinct differences in buyer behavior across cropland, pasture, and recreational/timberland.

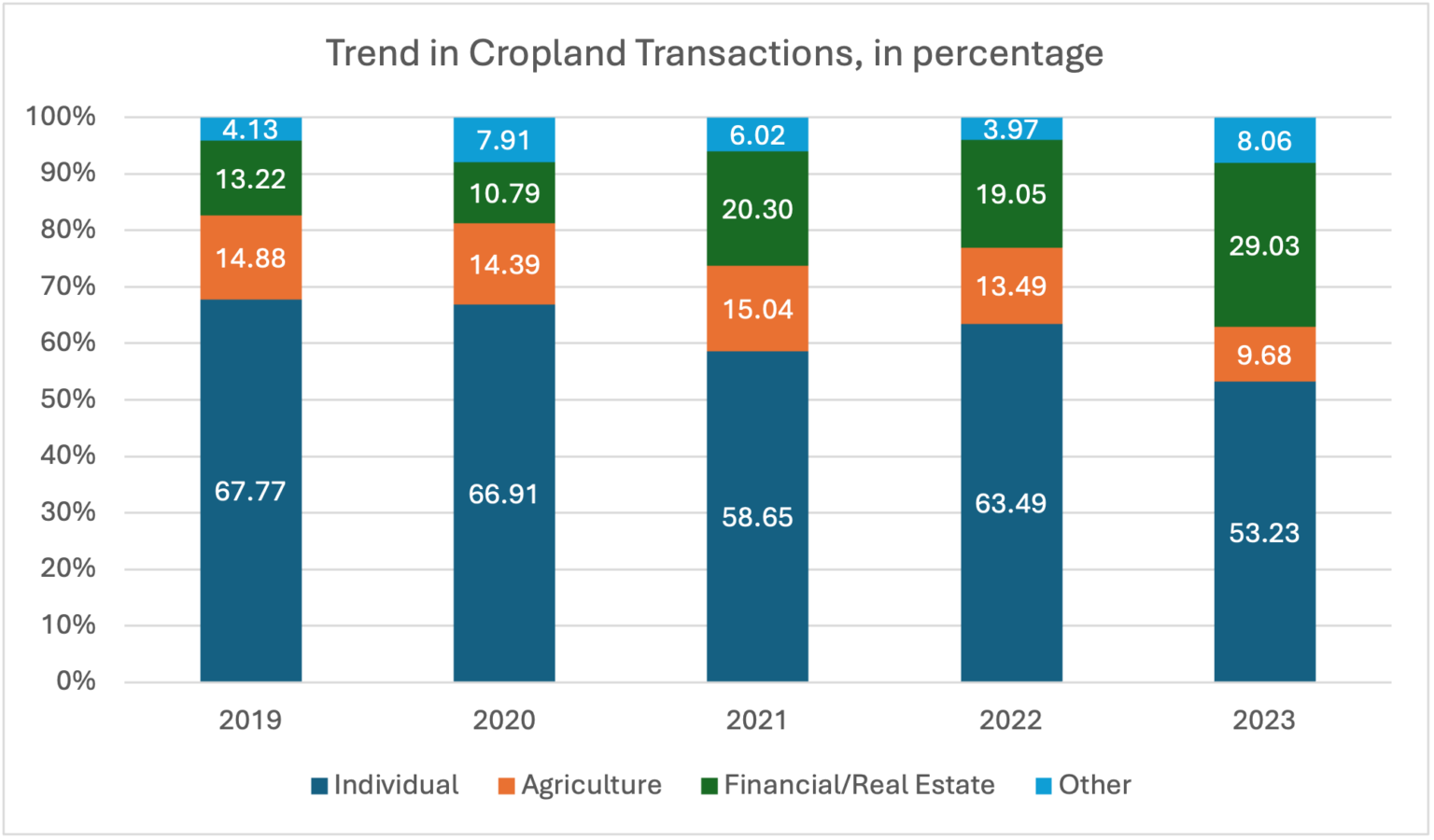

Cropland

Click here to see more...