By Joseph Glauber

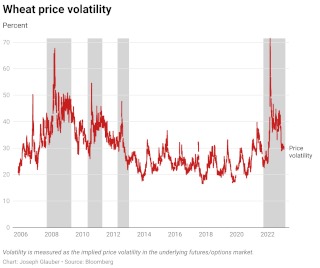

The Russia-Ukraine war has caused significant price volatility in agricultural markets over the past year—for wheat, in particular, price levels and price volatility reached the highest levels since the 2007/08 marketing year. Both have fallen back to pre-war levels over the past six months, but volatility remains high relative to historical levels (Figure 1), indicating that significant market uncertainty remains, creating ongoing vulnerability for global food security.

Before 2022, volatility (measured by the implied volatility in the wheat futures market) spiked and remained high three times since 2006—in 2007/08 and then again in 2010/11 and 2012/13 (as indicated in the grey bands in the figure). Markets then remained relatively quiet until the recent spike following Russia's invasion of Ukraine in February 2022. High volatility persists due to market uncertainty over the war and the relative tightness in stock levels, which provide little cushion against unforeseen production shortfalls.

Price volatility can, in part, be traced to uncertainty over the continuing flow of supplies, which depends on a number of factors, principally current production and existing stocks. This blog post focuses on the latter, examining the link between global wheat stocks and price volatility, as well as how—and how much—the tightness in global stocks over the past 18 months has exacerbated volatility, and prospects going forward.

Explaining global stocks

Stocks are crucial for buffering the impacts on market prices caused by production shocks such as droughts, extreme weather, conflicts, or other disruptions. When production shortfalls occur, available inventories can help to tide markets over until the next harvest, thus moderating price impacts. Conversely, when global harvests are large, wheat can be carried forward for sale in the next marketing year, thus putting an effective floor on current prices. In this way, stocks help moderate price peaks and troughs and thus reduce price volatility. However, when stocks are at already low volumes, as they have been over recent months, the capacity to buffer the impacts of shocks is more limited.

Tracking global wheat stocks, and their connection to market price volatility, is complicated. Measurements are typically based on aggregating country ending stocks (often called carryover stocks), the amount held at the end of a marketing year before the new crop is harvested and available for consumption. A country's ending stocks are equal to the previous year's ending stocks, plus any new production and imports, minus what is consumed domestically and exported during the year. In general, world stocks refer to the global sum of ending stocks at the close of each country's national marketing year. Because the dates of marketing years may vary across countries due to differences in local crop calendars, estimates of global ending stocks are not an actual measure of available stocks at a particular point in time, but serve more as an indicator of the level of current supplies that will be carried into the next marketing year.

Countries with public stockholding programs account for about 65% or more of global wheat stocks. Public stocks are held by governments for food security purposes, to bolster producer income, or both. Globally, the balance of publicly held stocks has shifted in recent years from the United States and European Union to other countries, notably China and to a lesser extent India. Historically, the U.S. and EU maintained large wheat reserves as part of their price support programs, but policy reforms in the 1980s and 1990s eliminated those programs. More recently, public stockholding schemes like the Food Corporation of India and the Chinese state-owned food company COFCO have bought, sold and stored large quantities of wheat and other grains.

The remaining third or more of global stocks are held by private and commercial entities (including individual farmers). A distinction is often made between private stocks held for discretionary purposes (sometimes called "speculative" stocks) and so-called "pipeline" or "working" stocks. Discretionary stocks are held by commercial interests that purchase grain in one period with the hope of selling later at a price high enough to recoup the costs of purchasing and storing the crop. Pipeline stocks are stocks held for operation of the marketing chain and are generally less price responsive than discretionary stocks.

Unfortunately, the diversity of governments and private entities involved means data on global stocks are incomplete and often of poor quality, meaning it is difficult to have complete confidence in world ending stock figures. Many countries (including some developed economies) fail to collect or publish data on stocks and thus analysts must impute the level of stocks based on production and consumption data. While improving the quality of stock data has been the focus of organizations like the Agricultural Market Information System (AMIS), much uncertainty remains over data quality. In addition, the physical quality of the stocks is often unknown. If stored properly, wheat can be held for several years, but if the quality deteriorates sufficiently, it may be unusable for milling purposes and must be used as animal feed or for industrial uses like biofuels.

How do stocks affect price volatility?

Typically, stocks serve to limit potential price impacts from rises and falls in production. In the event of a bumper crop, private storers purchase grain with the intention of selling it in the next period for an expected profit. This effectively puts a floor on market prices. Likewise, when stocks carried forward from the previous year are high and there is a production shortfall, storers will sell grain rather than carrying it forward to the following year. This helps moderate prices and buffers the impact of the production shortfall.

But the current global market environment—with its combination of post-pandemic effects, droughts, impacts from the war, and other issues—is anything but typical, has led to generally tighter stocks. When stocks are tight the ability of storers to buffer production shocks is limited. When discretionary stocks are limited and a production shock occurs, holders of pipeline stocks (such as millers) are reluctant to release the grain to ensure adequate supplies for milling and other users. Yet consumers often are willing to pay more for scarce grain supplies, giving up other expenditures (see this recent post by Abay, Karachiwalla, Kurdi and Salama on the impacts of food price shocks on diets of Egyptian households). Thus, prices keep rising; only large price increases can reduce demand sufficiently to meet the full impact of a supply shock. As a result, the price volatility tends to be far higher when stocks are low.

Click here to see more...