By Michael Langemeier

Fed cattle prices have increased dramatically in the last several weeks. In September, fed cattle prices for steers in Kansas averaged $101.23 per cwt. At the end of 2019, fed cattle prices were $122.00. This increase in fed cattle prices had a large impact on cattle finishing profitability in the fourth quarter of 2019. Moreover, fed cattle prices are predicted to remain strong through at least the second quarter of 2020. This paper discusses trends in feeding cost of gain, the feeder to fed price ratio, and net returns, and examines net return prospects for the next several months.

Several data sources were used to compute net returns. Average daily gain, feed conversion, days on feed, in weight, out weight, and feeding cost of gain were obtained from monthly issues of the Focus on Feedlots newsletter (here). Futures prices for corn and seasonal feed conversion rates were used to project feeding cost of gain for the next several months. Net returns were computed using feeding cost of gain from monthly issues of the Focus on Feedlots newsletter, fed cattle prices and feeder cattle prices reported by the Livestock Marketing Information Center (LMIC) (here), and interest rates from the Federal Reserve Bank of Kansas City.

Feeding Cost of Gain

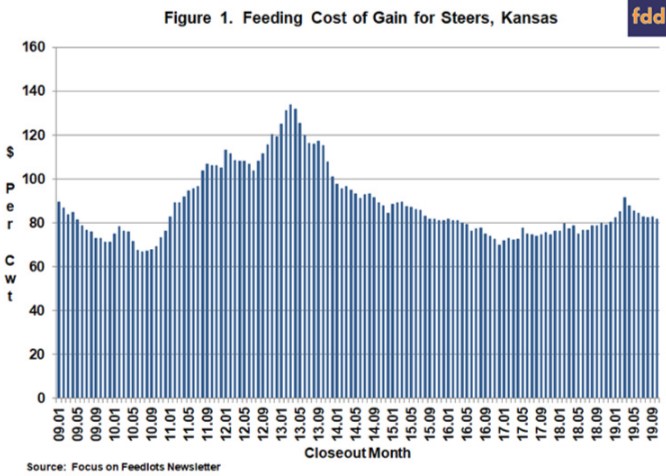

Figure 1 illustrates monthly feeding cost of gain from January 2009 to October 2019. Feeding cost of gain averaged $78.10 per cwt. in 2018 ranging from a low of $74.87 in May to a high of $80.31 in December. During the first 10 months of 2019, feeding cost of gain ranged from $81.61 in October to $91.67 in March, and averaged $84.64. Given current corn and alfalfa price projections, feeding cost of gain is expected to range from $80 to $83 for the first six months of 2020. Feeding cost of gain is sensitive to changes in feed conversions, corn prices, and alfalfa prices. Regression analysis was used to examine the relationship between feeding cost of gain, and feed conversion, corn prices, and alfalfa prices. Results are as follows: each 0.10 increase in feed conversion increases feeding cost of gain by $1.43 per cwt., each $0.10 per bushel increase in corn prices increases feeding cost of gain by $0.87 per cwt., and each $5 per ton increase in alfalfa prices increases feeding cost of gain by $0.55 per cwt.

Feeder to Fed Cattle Price Ratio

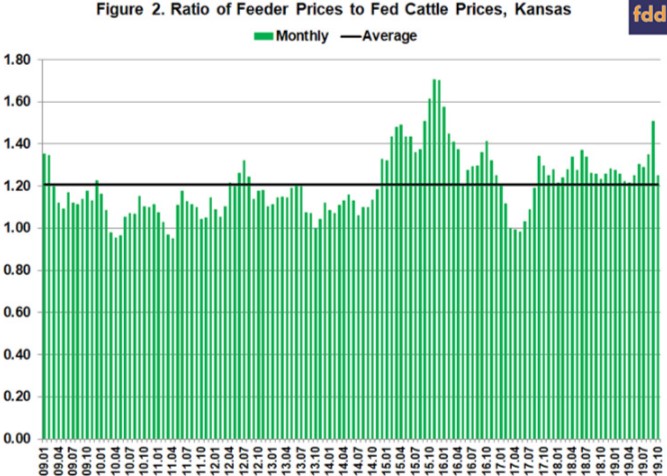

The ratio of feeder to fed cattle prices since 2009 is illustrated in Figure 2. During the ten-year period, this ratio averaged 1.21. The feeder to fed price ratio was one standard deviation below (above) this average for 16 (17) months during the ten-year period. The average net return for the months in which the ratio was below one standard deviation of the average was $135 per head. In contrast, the average loss for the months in which the ratio was above one standard deviation was $256 per head. The average ratio for the 17 months with a feeder to fed price ratio that was above one standard deviation of the ten-year average was 1.49. The feeder to fed cattle ratio was 1.51 in September, resulting in large losses. Since September, this ratio has been substantially lower, averaging 1.22 in December. Given current price projections, the feeder to fed price ratio is expected to average 1.17 in the first quarter and 1.19 in the second quarter of 2020. Though much lower than the levels experienced in September, the ratios for the first two quarters of 2020 are still not one standard deviation below the mean. Unless fed cattle prices are well above projected levels ($123 per cwt. in the first quarter of 2020 and $121.50 per cwt. in the second quarter of 2020), net returns are not expected to exceed $100 per head during the first six months of 2020.

Net Return Prospects

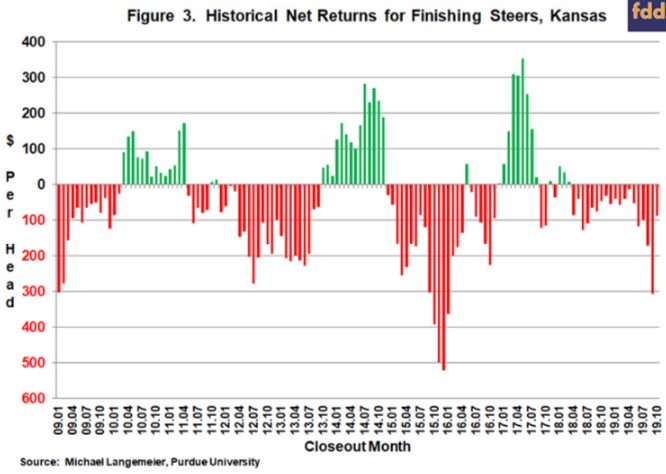

Monthly steer finishing net returns from January 2009 to October 2019 are presented in Figure 3. It is important to note that net returns were computed using closeout months rather than placement months. Net returns averaged $111 per head in 2017 and a negative $45 per head in 2018. Net losses for the first six months of 2019 averaged $52 per head. For the third quarter of 2019, net losses averaged $191 per head. Estimated net losses for the fourth quarter of 2019 are expected to range from $10 to $40 per head.

Before examining net return prospects for the next six months, we will discuss breakeven prices. Historical and breakeven prices for the last ten years, as well as projected breakeven prices through the first six months of 2020, are illustrated in Figure 4. Breakeven prices in the first six months of 2020 are expected to range from $119 to $122 per cwt. with the highest breakeven prices expected to occur in March and April. Given current fed cattle price projections, net returns are expected to range from -$20 per head in April to $50 to $60 per head in January and February. If the net returns in January and February materialize, they will represent the strongest net returns since early 2018.

Conclusions

This article discussed recent trends in feeding cost of gain, the feeder to fed price ratio, and cattle finishing net returns. Average cattle finishing losses in 2019 are estimated to be approximately $80 per head. Current breakeven and fed cattle price projections suggest that the long period of red ink stretching back to early 2018 is coming to an end. The average net returns for the first six months of 2020 are expected to be above breakeven levels. Net return projections for the next few months are primarily driven by the feeder to fed price ratio. A spike in fed cattle prices during the next few months would have a large impact on net return projections. Previous analysis suggests that each 0.01 change in the feeder to fed cattle ratio results in an $8.63 change in net returns. It is not uncommon for the feeder to fed cattle price ratio to change from 0.05 to 0.10 in consecutive months.

Source : farmdocdaily