By Don Shurley

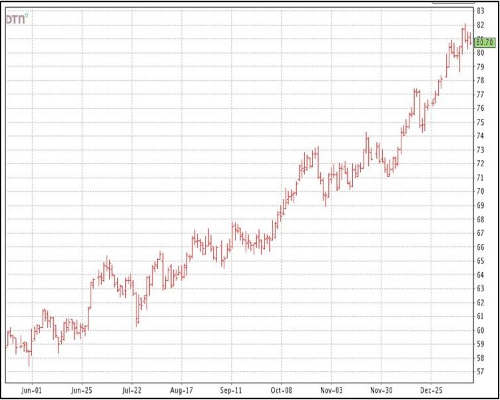

Old crop March futures pushed above 81 cents this week. New crop December topped 77 cents. Old crop was down a little to close out the week, but cotton enjoyed another good week due to several positive reports released.

March gained 0.93 cents for the week (down 0.45 today), 2.58 cents so far for the month, and 9.59 cents since December 3rd. Price is now the highest in over 2 years—since September 2018. Should prices continue to trend up, there will be “resistance” at 83 cents. There should now be “support” at 77 and again at 74.

As prices have improved, hopefully growers have taken advantage of the opportunities at multiple levels to achieve a good overall average price. Looking back, you may now regret pricing at 72 or 74 or 78, but no one knows where price is headed and one marketing approach is to sell as the market improves hoping to do better (scale up) each time.

USDA’s supply/demand estimates were released on Tuesday this week. The market was/is looking for signs of improved demand/Use and an overall tightening supply/demand picture. This week’s numbers were encouraging.

- The 2020 US crop was trimmed another 1 million bales, from the December estimate, and now stands at 14.95 million bales. This is over 3 million bales less than the first estimate back in March.

- US exports for the 2020 crop year were raised 250,000 bales from the December projection.

- To have a large cut in the crop (less available supply) and also to have an increase in exports at the same time is especially positive for the overall supply/demand picture.

- This results in a large draw down in US ending stocks to 4.6 million bales, compared to 5.7 last month, and 7.25 for last year.

- World production down due to US reduction and also a 200,000 bale decrease for Pakistan. No change for China. Turkey and Australia each increased 100,000 bales from the December estimate.

- World Use increased 100,000 bales from the December estimate. China Use was increased ½ million bales, Turkey 200,000 bales. Use for Vietnam was down 100,000, and Indonesia down 200,000 bales.

The run-up in price is due mostly to improved optimism in demand. Yes, the smaller US crop has also been a factor. Should news turn negative, the market has support at 77-78 and lower at 74. The market should continue strong, as long as the signals confirm what has fueled the run-up—a recovery in demand/Use.

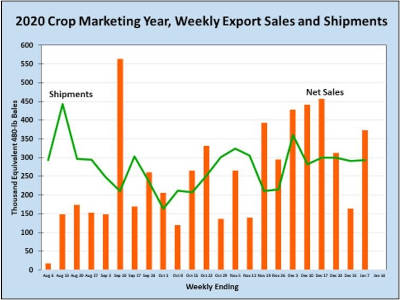

This week’s export report (for the previous week ending January 7th) was strong and also helped support the market. Net sales for the week were 372,800 bales and shipments were 293,400 bales. Sales were more than double the prior week with 44% to China. Large buyers also included Pakistan, Turkey, Vietnam, and Bangladesh. Shipments included 56% to China.

Optimism continues to reign, but there are economic, political, and trade uncertainties and cautions ahead that could sidetrack prices for both remaining old crop and the new crop. The new crop contract is at 77 basis December, or a Put locks in a floor of mostly 70 to 71 basis December, depending on the Strike Price. As we move forward, be alert and carefully evaluate alternatives.

Source : ufl.edu