By Fred Gale

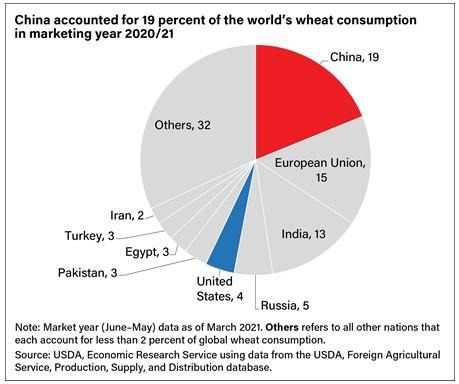

As the world’s largest wheat market, China accounted for an estimated 19 percent of the world’s wheat consumption in marketing year 2020/21 (July–June). That’s more than the European Union’s 15-percent share, and far ahead of the 4-percent U.S. share (see chart below). To meet demand for a population of more than 1.4 billion, China imports wheat, but at a volume less than half of what is allowed under a quota system first established when China joined the World Trade Organization (WTO) in 2001. A study by USDA’s Economic Research Service (ERS) looked at China’s past procedures for allocating quotas to its prospective importers and revealed that, based on the application rates for wheat quotas, demand for imported wheat often exceeded what was typically awarded. ERS’ analysis of China’s wheat import data suggests that import volume in 2021 is poised to reach that quota for the first time in two decades.

Embed this chart

Download larger size chart (2049 pixels by 1724, 144 dpi)

While China may be known for its consumption of rice, wheat flour is the main ingredient in many of the country’s staple foods, such as steamed bread, noodles, scallion-filled pancakes, deep-fried dough, and dumplings in heavily populated northern regions. More recently, flour-based instant noodles, European-style breads and pastries, hamburger buns, and snack foods have become popular all over the country.

Since the 1990s, China’s wheat market has progressed. It was once composed mainly of subsistence farmers, government-run procurement stations, and rudimentary flour mills. Today, China’s wheat farms are still small in scale, but nearly all wheat is mechanically harvested, and farmers sell most of their wheat. They can sell to traders or warehouses, choosing the buyer that offers the best price. Some village-run flour mills have morphed into nationally known companies. Flour is sold in supermarkets and used by bakeries and food processors. Consumers can find bread, noodles, and snack foods in fast-food kiosks, shopping-mall bakery chains, and workplace cafeterias.

Market Opened Less Than Expected

While China’s industry has changed considerably over two decades, the current quota system continues to reduce Chinese flour millers’ access to overseas wheat suppliers. In part because wheat is a staple food crop, the Chinese government has tightly controlled the wheat market for decades. Until the 1990s, China’s wheat imports were monopolized by a state-owned grain-trading company, China Oil and Foodstuffs Corporation (COFCO), which bought and sold wheat based on orders from government planners.

When China joined the World Trade Organization in 2001, authorities agreed to establish a tariff-rate quota (TRQ) that was meant to open the China wheat market to import business and reduce the government’s monopoly (see blue box below). Under the TRQ, China now allows up to 9.636 million metric tons (the quota) to be imported at a 1-percent tariff. Imports in excess of the TRQ can be imported with a 65-percent wheat tariff applied, but it is usually not profitable for millers to import wheat when this tariff is applied.

Because China originally expected demand for quotas to exceed availability, the government established a mechanism to award quotas. Companies interested in importing wheat must apply for the quota in September of the year before they plan to import. A central government agency then decides which applicants will be awarded quotas and distributes certificates before January.

Although China lifted the monopoly on wheat imports when it joined the WTO, 90 percent of the wheat imported under the tariff-rate quota is set aside for end users who must import through a state trading enterprise (STE) designated by the Chinese government. This STE is the same company that once monopolized grain trade—COFCO—and the agency that assesses the quota applications is the same one that issued import orders to that company until the 1990s. The remaining 10 percent is reserved for importation through other entities with rights to import wheat.

Over the last 20 years, as China’s annual wheat use grew from about 110 million metric tons (Mt) to 145 Mt, the 9.636-Mt quota was unchanged. Imports never reached the quota, despite the apparent profitability of imports and robust demand for classes of wheat that are scarce in China. Despite indications of strong demand for imported wheat, China’s wheat imports were 3 to 5 Mt in most years, less than half the quota. Imports surged to nearly 8.4 Mt in 2020, the largest volume since the 1990s, but still fell short of the quota.

Imports of U.S. wheat were less than 1 Mt in all but a few years (note that the TRQ system does not specify the source of the wheat). Wheat imports surged during 2004 to stem rising Chinese grain prices that year and in 2013 to restock government reserves. Imports of U.S. wheat were especially low during 2018 and 2019, when China assessed retaliatory tariffs on U.S. commodities. Wheat imports from the United States experienced a resurgence in 2020 after the U.S.-China Phase One trade agreement, but China’s imports from France, Canada, Australia, and Lithuania also surged that year.

Embed this chart

Download larger size chart (2049 pixels by 1616, 144 dpi)

China’s delegation to the WTO has fielded many questions from counterparts about how the TRQs were administered, their opacity, and why the quotas were not filled. China’s TRQ mechanism, in place since 2001, had remained mostly unchanged until the United States initiated a WTO dispute that challenged the administrative practices China used to manage wheat, corn, and rice TRQs. In 2019, a report issued by a WTO Dispute Settlement Body found, among other things, that some of China’s procedures for allocating quotas were not transparent, predictable, or fair to applicants. The WTO report also revealed that Chinese authorities had used criteria to assess applications that were not revealed to the applicants. The report also indicated that the entire 90-percent state trading enterprise share of the quota had been set aside for use by COFCO, which did not have to follow application procedures, nor did it have to return unused quota as other applicants were required to do.

Shortly after the WTO issued its report, China revised application instructions to the 2020 TRQ that allowed applicants to request both STE and non-STE quota and stipulated new capacity requirements for applicants. COFCO’s headquarters appeared on the list of TRQ applicants for the first time in 2020. Despite these changes, WTO member countries remained unclear as to whether the revisions addressed issues raised in the dispute, as Chinese authorities did not reveal whether changes in procedures complied with requests made in the WTO report.

Applicants Seek Imported Wheat

In 2015, the Chinese agency handling TRQ applications began to post lists of quota applicants on its website. While the lists do not reveal how much quota was requested or received by companies, the number of applicants is an indicator of strong demand for imports. Hundreds of Chinese flour mills, food processors, trading companies, and feed mills apply for a share of the wheat import quota annually. The number of companies applying to import wheat in 2017 rose as high as 475, while the lowest number was 347 in 2020. More than 900 companies applied for the TRQ at least one year from 2015 to 2021, and 171 companies applied in all 7 years.

Most applicants are flour-milling companies that report a combined milling capacity of more than 100 Mt which, in aggregate, represent about half the industry’s total. By comparison, China’s national wheat imports of 3 to 4 Mt in most years are a small fraction of the industry’s milling capacity.

Data show that applicants who are awarded quotas receive small allocations. A few city-level offices in China announced that only one or two companies in their districts received quota allocations of a few hundred metric tons of wheat. By comparison, international wheat shipments are commonly transported in vessels with a capacity of 60,000 metric tons or more.

The quota applicants are a diverse group that reflects the makeup of China’s flour-milling industry. Three major companies listed below represent the diversity:

- Wudeli is a private company based in a wheat-growing area of Hebei Province that is now one of the four biggest millers in China: 25 branches submitted 81 applications for quotas in 2015–21.

- COFCO is the state-owned company that is now one of the world’s biggest grain traders. COFCO includes its Beijing headquarters and local flour-milling subsidiaries that apply for a share of the quota: 20 branches submitted 72 applications for 2015–21.

- Yihai Kerry is part of a Singapore-based multinational conglomerate that has grain and oilseed-processing businesses in China: 20 branches submitted 106 applications for 2015–21.

Most applicants for wheat quota are privately owned mills that were established several decades ago to mill local wheat. A few, like Wudeli, have expanded rapidly and built modern facilities with milling capacity exceeding 1 Mt. Many others are small scale and still conduct most business locally.

Besides COFCO and its subsidiaries, at least 25 other state-owned companies have applied for wheat TRQ. Some are trading companies operated by local governments responsible for ensuring city or provincial grain supplies. Grain reserves in some regions managed by such firms appear to be stocked partly with imported wheat. Other state-owned applicants are engaged in foreign agricultural development, are companies affiliated with state farms, or are entities engaged in agricultural marketing. Some Chinese government documents call for using state trade enterprise TRQs to implement trade initiatives, such as buying more wheat from Central Asian countries.

Despite Large Application Numbers From Wheat-Growing Regions, Other Companies Import Most of the Wheat

China’s flour-milling industry is highly competitive. Some milling companies have expanded rapidly even as the size of China’s flour market has remained relatively stagnant leading many in the industry to report low profit margins and excess capacity.

While no public information is available on which quota applicants import wheat, there are indications that not all companies are given equal consideration. Minimum production capacity requirements for quota applicants may preclude smaller plants from importing wheat. A comparison between the regional breakdowns of quota applicants and wheat imports indicates companies in wheat-growing regions have reduced access to wheat that can be imported under the TRQ.

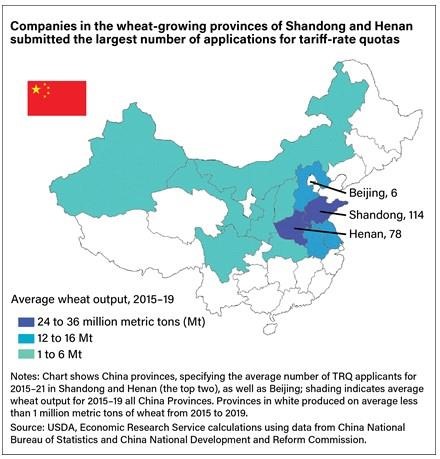

Three-fourths of TRQ applications are from companies in wheat-growing provinces of northern and western China (see map below). The top two wheat-growing provinces, Shandong and Henan, typically submit the largest number of TRQ applications. This is consistent with industry data indicating that about 90 percent of China’s flour-milling capacity is in wheat-growing provinces. Flour mills tend to locate near raw materials, and flour consumption is predominant in wheat-growing areas.

Embed this chart

Download larger size chart (2049 pixels by 2124, 144 dpi)

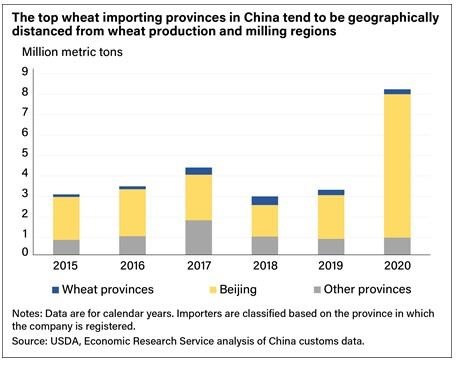

Wheat-growing provinces consistently accounted for about three-fourths of TRQ applicants, but Chinese customs data indicate these provinces account for an average of just 10 percent of wheat imports (see chart below). Instead, companies outside the wheat-growing regions are the primary importers of wheat in China. Beijing-based companies comprise the majority, with 69 percent of wheat imports, reflecting the predominance of COFCO, whose headquarters is in Beijing (few flour-milling companies are based there). Beijing companies’ share of imports increased to 87 percent in 2020, even though they accounted for 6 of 362 TRQ applications submitted. Other top importers are based in Guangdong and Fujian provinces, southern coastal regions where wheat is not grown in significant quantities.

Information from China indicates Beijing-based companies store imported wheat in various facilities around the country or sold on to other companies. However, steering imports to certain companies also gives those companies favorable profit margins denied to companies in wheat-growing areas that are not awarded wheat imports under the TRQ.

Embed this chart

Download larger size chart (2049 pixels by 1616, 144 dpi)

Feed Use Could Push Wheat Imports Past Quota

Chinese officials say their TRQ system is necessary for managing wheat supplies because tightly controlled food grain markets are vital to national security. But it may be the demand for wheat in animal feed, rather than for food, that may cause the wheat TRQ to fill in 2021 for the first time.

China’s wheat imports reached 7.2 Mt in the first 7 months of 2021, up 50 percent from the same period a year earlier. USDA estimates of market year imports for China suggested the pace would continue through the end of the calendar year, and wheat imports could reach the TRQ of 9.636 Mt in 2021.

China’s National Grain and Oils Information Center (CNGOIC), the premier grain analysis arm of the Chinese government, partly attributed increased wheat imports in marketing year 2020/21 to China’s commitment to buy U.S. products as part of the Phase One agreement. However, China’s customs data indicate that most of the increase in imports came from countries other than the United States.

Further, supply and demand estimates indicate that a surge in feed use of wheat was the most prominent change in China’s wheat market in the most recent marketing year. China’s wheat harvest was historically high, and flour mill demand increased only marginally. However, CNGOIC and USDA estimated demand in the “feed and residual” category increased 21 to 22 Mt in 2020/21.

In 2020, corn prices in China rose above those for wheat. This wheat-to-corn price inversion prompted widespread substitution of wheat for corn in livestock feed in China during 2020/21. Chinese authorities held numerous sales of wheat reserves to satisfy the demand for feed wheat. According to CNGOIC and other sources, some imported wheat was also used for animal feed.

The increase in feed use of wheat raises more questions about the TRQ’s operation and its future role. The wheat TRQ application guidelines stipulate minimum capacity requirements for flour mills and for food processors but nothing for feed mills. Some animal feed companies nevertheless applied for wheat TRQ, but their numbers dwindled from 31 in 2015 to 2 in 2020 and 8 in 2021. Branches of some of China’s largest feed companies appeared on the lists.

Source : usda.gov