By Michael Langemeier

Center for Commercial Agriculture

Purdue University

A contingency plan is a course of action designed to help a business determine how to respond to possible future events. Contingency plans are often referred to as “Plan B”. One of the most common contingency plans used by a business, particularly a small business, relates to how to respond to the departure or absence of key personnel. Contingency plans related to how to respond to changes in projected cash flows are also important. This article discusses how to use contingency plans to respond to cash flow shortages resulting from relatively low productivity, or crop or livestock prices.

Sources and Uses of Funds

In addition to providing a mechanism for reporting how a farm’s performance during an accounting period influenced and was influenced by major funding activities, a sources and uses of funds statement is useful when developing contingency plans. Specifically, this statement can be used to examine whether the farm has enough cash flow from the farm to repay debt and purchase assets. An example of a sources and uses of funds statement using historical data is illustrated and described by Langemeier (2019). A pro-forma spreadsheet that projects net farm income, sources and uses of funds, repayment capacity, and working capital can be found

here.

The five primary categories of a sources and uses of funds statement are beginning cash balances, cash flows from operating activities, cash flows from investing activities, cash flows from financing activities, and ending cash balances. Cash flows from operating activities are computed by subtracting cash farm expenses, owner withdrawals (e.g., family living withdrawals), and income and self-employment taxes from cash farm receipts. Cash flows from investing activities are computed by subtracting capital asset purchases from capital asset sales. If a farm is planning on purchasing assets, cash flows from investing activities will be negative. In other words, cash flows from operating activities or from financing activities will need to be used to help pay for the assets. Cash flows from financing activities are computed by subtracting principal payments from loans received during the year. If principal payments are higher than loan receipts, cash flows from financing activities are negative. Conversely, if principal payments are smaller than loan receipts, cash flows are positive.

Financial metrics and sources and uses of funds for a case farm will be examined below using a pro-forma spreadsheet (

here). To use the pro-forma spreadsheet the following information is needed: current assets, current liabilities, crop acres, crop income (bushels in storage, crop prices, and crop yields), other income (e.g., beef income), crop and livestock expenses per acre or head, assets sales and purchases, and nonfarm income and expenses (e.g., family living expenses). When conducting a pro-forma analysis, it is common to use more than one scenario. For example, Langemeier (2018) used three scenarios to examine the impact of changes in interest rates on financial metrics. In this article, we will use three crop price scenarios for sales this fall and ending inventories. The price scenarios were developed using historical basis and futures prices. For futures prices, the 25% percentile, the 50% percentile, and the 75% percentile for corn and soybeans were obtained in early April from the iFarm Price Distribution Tool (

here). Cash prices were then computed by adding historical basis to futures prices.

Case Farm Example

Let’s use the cash flow definitions above to look at an example. The case farm is located in southwest Indiana and has crop acres and a small beef cowherd. Gross revenue and net farm income in 2019 were $537,905 and $46,659, respectively. The operating profit margin in 2019 for the case farm was 4.7 percent. The farm has solid liquidity and solvency positions. Due to tight cash flows, the case farm has purchased very little machinery during the last few years. The farm wants to examine whether it would be possible to purchase $150,000 in machinery and equipment later this year.

There are least four different sources of cash that can be used to purchase machinery and equipment. Having said that, it is likely that a combination of these sources would be utilized. First, the farm could draw down cash balances. This would reduce liquidity, which may not be prudent. Second, the farm could use cash flows from operating activities, assuming that this number is positive. Third, the farm could sell other assets to help make the purchase. Fourth, the farm could borrow money to help pay for the asset. Where does contingency plans come in? If cash flow becomes relatively tight as the year progresses (as an example, suppose that crop prices are 10 percent below their expectations), cash flows from operating activities may be relatively small. In this instance, should the farm go ahead a make the $150,000 investment? The answer will depend on net farm income prospects which are examined below.

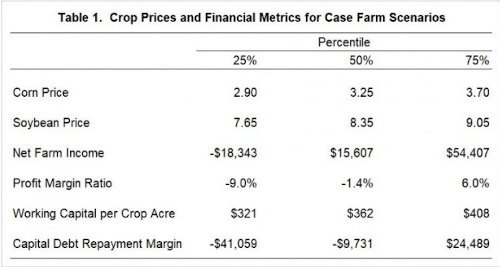

Table 1 presents crop prices and financial metrics for each crop price scenario. The only difference between the scenarios are the expected crop prices for fall sales and ending inventories. Net farm income, the operating profit margin ratio, and the capital debt repayment margin were negative for the low price scenario. The negative capital debt repayment margin indicates that this farm does not have enough cash flow from operating and financing activities to fully cover principal and interest payments on noncurrent debt. Working capital per crop acre declined from $375 in the beginning of the year to $321 at the end of the year for the low price scenario. For the medium price scenario, net farm income is $15,607, but the operating profit margin ratio and the capital debt repayment margin are still negative. Working capital per acre dropped $13 for the medium price scenario. For the high price scenario, net farm income, the operating profit margin ratio, and the capital debt repayment margin were all positive, and working capital per acre increased by $33.

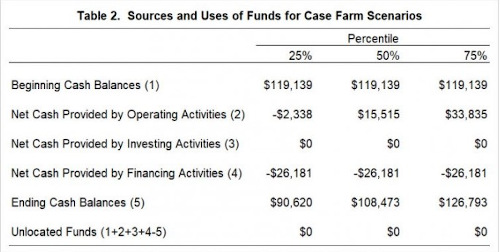

The primary categories for projected sources and uses of funds are illustrated in Table 2. The net cash provided by investing activities excludes potential asset sales and purchases. Net cash from operating activities was negative for the low price scenario, and was $15,515 and $33,835 for the medium price and high price scenarios, respectively. Note that depreciation, because it is a non-cash expense, is not subtracted from cash farm receipts when computing net cash provided by operating activities. Depreciation is projected to be approximately $55,000 in 2020. Thus, to a large extent this farm will be living off of depreciation in 2020. The ending cash balance was lower than the beginning cash balance for the low price and medium price scenarios. For the high price scenario, the ending cash balance was approximately $7,650 higher than the beginning cash balance.

Now let’s use the information in tables 1 and 2 to determine whether the case farm should purchase $150,000 worth of machinery and equipment later this year. If the farm wants to have a down payment of 25 percent or higher on new machinery, given that cash balances declined during the year, it would not be prudent to purchase the machinery and equipment under the low price and medium price scenarios. Under these scenarios, the case farm needs to have a plan for how it’s going to repay principal on noncurrent debt. Cash balances increased in the high price scenario, but not by very much. The case farm could afford to purchase the machinery and equipment under this scenario, but still may want to hold off so that it could preserve working capital.

Summary and Conclusions

This article briefly discussed contingency planning when cash flow becomes tighter than originally projected. As cash flows from the farm operation become tighter, it is necessary to find other funds to help pay for asset purchases or delay asset purchases, and to repay debt. A case farm was used to illustrate how contingency plans could be used. Unless crop price prospects improve it would be difficult for the case farm to purchase assets, such as machinery and equipment, later this year.

Source : illinois.edu