By Gary Schnitkey, Krista Swanson, Ryan Batts

Department of Agricultural and Consumer Economics

University of Illinois

and

Carl Zulauf

Department of Agricultural, Environmental and Development Economics

Ohio State University

This article documents the very late planting that is occurring in 2019, leading to the prospects of lower yields and higher than normal prevented planting from crop insurance. As a result, one suspects that corn prices will increase. For many farms, price increases are needed to cause planting corn to be an economical alternative to taking prevented planting. As of yet, prices have not risen enough to induce farmers to plant corn after the final planting date if all inputs still need to be applied. Paradoxically, rising prices could reduce Price Loss Coverage (PLC) payments for 2018, which will be received this fall.

Planting Progress

Currently, the National Agricultural Statistical Service (NASS) is reporting that 49% of the corn crop has been planted. This value is as of May 19 and is well below the 80% average progress for this week. It is the lowest value on record, dating back to 1980 when these statistics became available on Quick Stats. Next lowest progress is 56% in 1995.

Low planting progress is widespread across the greater Corn Belt, particularly the eastern Corn Belt:

- Michigan has 19% of its corn planted (54% five-year average, 23% was lowest progress at this week for any year since 1980, June 5 final planting date for crop insurance),

- Ohio has 9% of its corn planted (62% five-year average, 13% was lowest progress at this week for any year since 1980, June 5 final plant date),

- Indiana has 14% of its corn planted (73% five-year average, 13% was lowest progress at this week for any year since 1980, June 5 final planting date), and

- Illinois has 24% of its corn planted (89% five-year average, 20% was lowest progress at this week for any year since 1980, June 5 final planting date, except for southern Illinois).

Very slow planting also is occurring in some states in the western Corn Belt:

- North Dakota has 42% of its corn planted (63% five-year average, 17% was lowest progress at this week for any year since 2000, May 25 final planting date, except for May 31 in southeast counties), and

- South Dakota has 19% of its corn planted (76% five-year average, 17% was lowest progress at this week for any year since 1980, May 25 final planting date except for May 31 in southeast counties).

There are four states with over 50% of the corn planted. These states still lag five-year averages:

- Iowa has 70% of its corn planted (89% five-year average, 60% was lowest progress at this week for any year since 1980, May 31 final plant date),

- Nebraska has 70% of its corn planted (86% five-year average, 45% was lowest progress at this week for any year since 1980, May 25 final planting date),

- Minnesota has 56% of its corn planted (83% five-year average, 37% was lowest progress at this week for any year since 1980, May 25 final planting date in northern Minnesota and May 31 final planting date in central and southern Minnesota),

- Missouri has 62% of its corn planted (93% five-year average, 29% was lowest progress at this week for any year since 1980, various final planting dates),

In past years, planting progress for corn during any given week can be large. The largest progress across the 18 largest states was 43% in 2013. The maximum planting during the 21st week of the year is 20%, which occurred in 2009.

Conditions do not suggest rapid progress this week. The Midwest received a great deal of rain last week, with over 2 inches of rain across northern Illinois, much of Iowa, and western Ohio. These saturated soils will take time to dry out.

At best, weather forecasts do not suggest drying conditions over much of the Midwest. The 7-day precipitation forecasts from the National Weather Service (NWS) is projecting over 3 inches of rain in the western Corn Belt. Less rain is projected for the eastern Corn Belt. Still, if these rains materialize, progress could be halted, particularly in the western Corn Belt.

At this point, the following expectations seem reasonable:

- A significant portion of corn likely will be planted the last week of May or first week of June. While corn planted this late can yield well, below trend yields are more likely (see farmdoc daily, May 1, 2019).

- More than the usual number of corn acres will likely not be planted by the final planting date for crop insurance purposes. Dates are as early as May 25 for states in the Great Plains to as late as June 5 in the eastern Corn Belt (see farmdoc daily, May 7, 2019). It is quite possible that the May 25th final planting day will pass without much progress being made in the northern Great Plains.

- The potential exists for a record-breaking number of acres taking prevented planting payments. The most similar year to this in terms of planting progress is 1995. In 1995, crop insurance policies were very different than today. More acres are insured today and at higher guarantee levels, resulting in prevented planting payments looking more favorable now than in 1995.

- Much will depend on the weather this week and next. The 7-day forecast for the last week of May is of intense interest, particularly if the rains forecast for this week materialize.

Price Response

Corn prices have risen in recent days. For corn in Midwest states, the projected insurance price for corn is the average December settlement prices of Chicago Mercantile Exchange (CME) contracts during February. The 2019 projected corn price is $4.00 per bushel. The December contract settled at $4.04 on May 20th, almost the same as the projected prices and well above the $3.72 low on May 9th. Note that these are futures prices. Cash and forward bid prices are considerably lower. In central Illinois, fall delivery bids are about $.25 per bushel lower than futures prices.

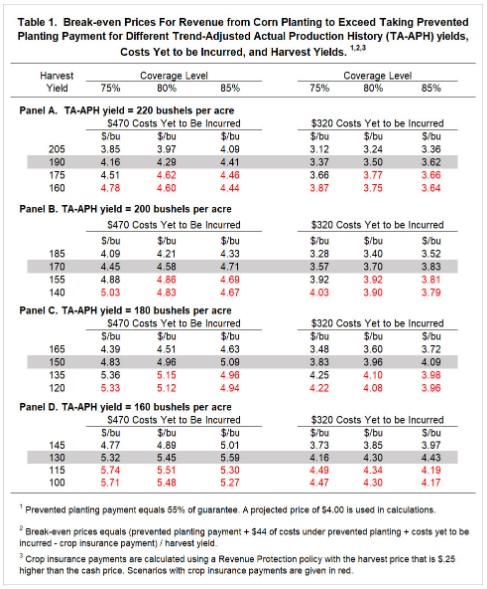

Break-even Corn Prices

A significant question is: Have corn prices risen enough to draw acres away from prevented planting once the final planting date arrives? To aid in answering the question, break-even cash corn prices that cause planting corn to have the same returns as taking prevented planting are presented in Table 1. Note, these are cash prices, not futures prices. Assumptions used in Table 1 are given in more detail in a

May 14th farmdoc daily article. Briefly those assumptions are:

- The prevented planting payment for corn is 55% of the guarantee. Farmers had the opportunity to buy-up to a 60% prevented payment factor. Increasing the payment factor will increase the break-even prices.

- $43 per acre of costs are incurred on a prevented planting acre.

- $470 per acre are costs left to be incurred if corn is planted (see farmdoc daily, May 14, 2019 for a list of costs). The $470 assumes that nitrogen and pesticides have not been applied and fieldwork has not been completed. Table 1 also includes a cost scenario of $320 per acre costs left to be incurred. This is based on having nitrogen and herbicide applied and some field work completed; with those expenses already paid there are fewer costs left to be incurred. Roughly, the field is ready to be planted with all nitrogen and herbicide applied.

- Table 1 gives break-even prices for different Trend-Adjusted Actual Production History (TA-APH) levels. Costs to be incurred are not varied for different TA-APH yields. Field passes and herbicide programs differ little between higher and lower productivity fields. Fertilizer and seed costs may decrease, but those cost decreases are relatively minor.

To illustrate the interpretation of Table 1, take a field with a TA-APH yield of 220 bushels per acre (Panel A). If no field work has been completed, nearly $470 per acre in costs have yet to be incurred. Break-evens for an 85% coverage level are $4.09 for a 205 bushel per acre yield, $4.41 for a 190 bushels per acre yield, and $4.46 for a 175 bushels per acre yield. Prices need to rise before planting corn is an economically-attractive option compared to not planting, especially as TA-APH yield declines.

Field trial work at the University of Illinois suggests that expected yields are between 80 and 85% of maximum yield when planting occurs in early June (farmdoc daily,

May 15, 2019). A decline of this nature would be roughly a 30 bushel per acre. Yields that are 30 bushels below the TA-APH are noted by a gray background in Table 1.

Yields lower than TA-APH can trigger crop insurance payments. In Table 1, break-even prices that include crop insurance payments are highlighted in red. Break-evens in Table 1 are calculated assuming the harvest price for crop insurance purposes is $.25 above the cash price using a Revenue Protection (RP) policy. Note that crop insurance payments stop the increase in the break-even price as yield decreases.

To provide more intuitions, Figure 1 shows the break-evens from Table 1 at the 85% coverage levels in graphical forms. Note several items:

- Break-evens increase with lower TA-APH because, by assumption, costs vary little with APH yield. Note that break-even prices are very high, even when some input costs have already been paid and there is a lower amount ($320) yet to be incurred. At a 75% coverage level, the break-even corn price is over $4.00 when yields are lower than 130 bushels per acre. These results suggest that lower productivity farmland will be more likely to take late planting.

- The higher the costs of planting yet to be incurred, the more likely prevent planting payments will be taken. When $470 of planting costs are left to be incurred, break-even cash prices are well over $4.00 given the lower expected yields from late planting. Farms who have not incurred any planting costs will require higher prices than the market is currently offering to make planting corn an economic alternative relative to not planting.

Corn Price Increases and 2018 Market Year Average Price

Higher prices in the summer months could increase the 2018 MYA price, resulting in lower payments for the 2018 crop by the Price Loss Coverage (PLC), Agricultural Risk Coverage at the county-level (ARC-CO), and ARC at the individual level (ARC-IC). This implication will be most directly felt by PLC, as ARC-CO is not likely to make payments (see farmdoc daily,

April 2, 2019). Lower PLC payments will not impact a large number of farmers, as only 6.6% of corn base acres are in PLC. Still, budgeting for lower payments for those farmers seems prudent.

Price estimates for the current market year are available in the World Agricultural Supply and Demand Estimates (WASDE) reports for May beginning with the report released in May 1977 for the 1976 market year. The corn market year starts September 1 and ends August 31. Changes in the current market year price estimates are examined from the May WASDE until the final price for the year is released, which occurs in the November WASDE. Note, the period of price change is over the growing season for the upcoming crop. The largest percent increase in market year price is +11 per-cent for the 1987 market year. This increase occurred during the drought-stressed growing period of the 1988 crop. Next largest increases are both +4% for the 1978 and 2001 market years. During the 2012 drought, the price for the 2011 market year increased +2%.

The recent 2019 May WASDE forecast a price for 2018 market year of $3.50, implying a potential PLC payment rate of $0.20 per bushel before adjusting for the sequestration amount and the 85% base acre payment factor. An increase of 5.7% would eliminate PLC payments. Such an increase has happened once. The 2% increase in price that happened during the 2012 drought would increase the 2018 market year price to $3.57, reducing PLC payment to $0.13 from $0.20.

Summary

For farmland that has no inputs applied, cash corn prices must exceed $4.00 by large amounts for planting to have the same expected returns as taking prevented planting other than for fields with very high expected yields and individual farm insurance coverage levels below 80%.

Farmers should complete their own analysis of plant and prevented planting alternatives on a field by field basis. As this article illustrates, the prevent plant decision is significantly impacted by expected yield, insurance coverage level, and planting costs already incurred. There is no universal decision rule. The farmdoc Prevented Planting Module can be used to aid in making these decisions. The Prevented Planting Module is part of the Planting Decision Model, a Microsoft Excel spreadsheet within the FAST series available for download on farmdoc (

here). The specific spreadsheet is available (

here).

Another consideration is trade aid currently being crafted for 2019. If the decision is to distribute based on 2019 production, prevented planting become less favorable. A

May 14th article entitled “Prevented Planted Decision for Corn in the Midwest” covers these issues).

When prevented planting becomes an option, we suggest farmers speak with crop insurance agents. There are additional risks to planting in terms of downside revenue risk and reductions in APH yields.