Oil Markets Tighten as Middle East Conflict Disrupts Supply and U.S. Production Ramps Up

Global energy markets have entered a period of heightened volatility, with ripple effects reaching well into the agricultural economy. The U.S. Energy Information Administration (EIA) has released its latest Short-Term Energy Outlook amid Middle East conflict.

From diesel and fertilizer costs to grain transportation and crop-drying expenses, energy prices remain a key factor influencing farm profitability. Recent developments in the Middle East and shifting U.S. production trends are reshaping the outlook for crude oil, natural gas, and electricity through 2027.

Below is a breakdown of EAI’s latest expectations and what they mean for North American agriculture.

Crude Oil Prices Surge Amid Middle East Conflict

Brent crude oil prices have climbed sharply in recent weeks. As of March 9, Brent settled at $94 per barrel, roughly 50% higher than at the start of the year and the highest level since September 2023.

The spike is primarily driven by:

- Reduced petroleum shipments through the Strait of Hormuz, a critical global shipping chokepoint.

- Shut-in oil production in the Middle East resulting from escalating military action.

Because the Strait handles a significant share of global oil flows, even short-lived disruptions can have outsized effects on global prices.

Middle East Production Outlook: A Temporary but Significant Disruption

Forecasting remains highly dependent on the duration and intensity of the conflict.

Current modeling assumes:

- Additional declines in Middle East oil output as the closure of the Strait of Hormuz continues to constrain exports.

- Production gradually recovering once transit through the Strait resumes.

Given these assumptions, energy markets may remain tense through the spring.

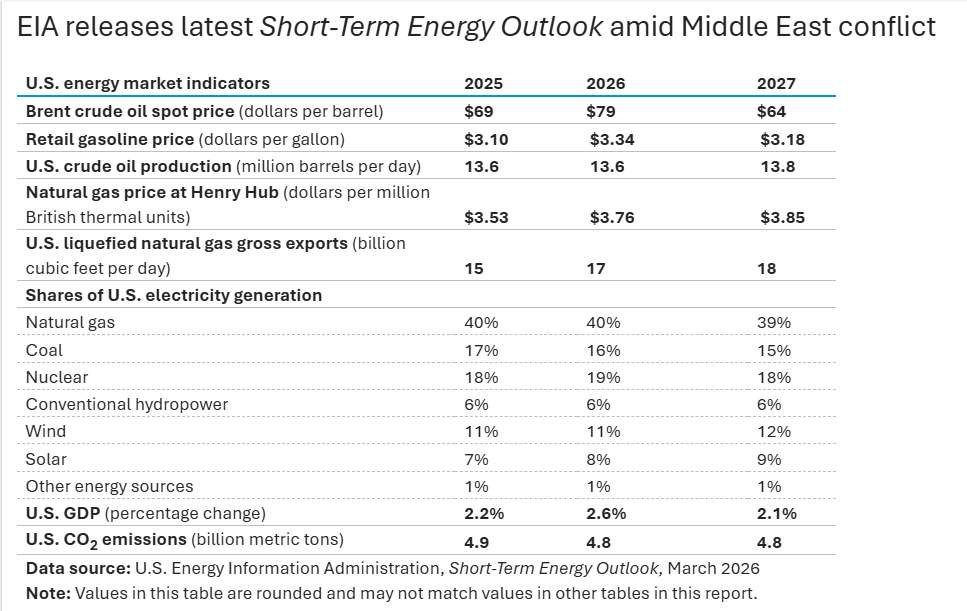

Crude Oil Price Forecast Through 2027

Analysts expect crude oil prices to remain elevated near-term before easing later in the year:

- Above $95/bbl for the next two months.

- Below $80/bbl by Q3 2026.

- Around $70/bbl by year-end 2026.

- Averaging $64/bbl in 2027.

These numbers carry significant uncertainty due to geopolitical risks. For farmers, this suggests continued short-term pressure on diesel and fuel-related costs, but a potential easing trend heading into late 2026 and 2027.

U.S. Oil Production Rising in Response to Higher Prices

Higher prices are prompting a supply response in the U.S. oil sector.

Forecasts call for:

- 13.6 million barrels/day (b/d) average production in 2026.

- 13.8 million b/d in 2027, which is 0.5 million b/d higher than last month’s projection.

This added production could help stabilize global supply once Middle East constraints ease.

Natural Gas Prices: Minimal Impact on U.S. Market

While reduced LNG flows through the Strait of Hormuz have lifted natural gas prices in Europe and Asia, the U.S. market remains largely insulated.

Henry Hub Natural Gas Forecast

- $3.80/MMBtu in 2026 (13% lower than last month’s forecast)

- $3.90/MMBtu in 2027 (12% lower than last month)

Two major factors are driving these revisions:

- Milder-than-expected February temperatures, leaving more gas in storage.

- More associated natural gas production, tied to increased U.S. crude output.

The result: Lower U.S. natural gas prices despite international turmoil.

Natural Gas Production and Inventories

Higher crude oil production is directly increasing associated natural gas output.

Forecasts now expect:

- 121 Bcf/d marketed production in 2026 (up 2% from 2025).

- 124 Bcf/d in 2027, nearly 2 Bcf/d higher than earlier estimates.

Storage levels are also stabilizing. Inventories at the end of the winter withdrawal season (March) are projected near 1,840 Bcf, close to the five-year average. This follows a February slowdown in withdrawals after extreme January cold tied to Winter Storm Fern.

Electricity Demand and Generation Trends

Electricity demand continues to rise across the United States, driven by population growth, electrification, and expanding data center energy requirements.

Key projections include:

- 1.2% electricity generation growth in 2026

- 3.1% growth in 2027, with the largest increases occurring in Texas (ERCOT) Renewables continue to expand their share of the generation mix. In 2026:

- Coal generation will decline by 7%

- Approximately 4% of coal-fired capacity is expected to retire

- Renewable output will increase accordingly

For farms, this may contribute to relatively stable electricity prices in the long run, though regional variations will persist.

What This Means for Farmers

Energy remains a major cost driver for farm operations—from diesel and propane to nitrogen fertilizer and electricity.

Based on current forecasts:

- Short-term diesel and fuel costs may remain elevated, but relief is expected later in 2026.

- Natural gas–based fertilizer costs may experience downward pressure, thanks to higher U.S. gas production and stable inventories.

- Electricity pricing likely to remain stable, with renewable growth offsetting coal retirements.

- Geopolitical risks remain the wild card and could disrupt energy markets quickly.